Market Dynamics & Rationale

Financing conditions for non-financial corporations (“Corporates”) shape developments in the real economy and are, inter alia, affected by monetary policy.

Financing structure of euro area Corporates changed since the financial and economic crisis:

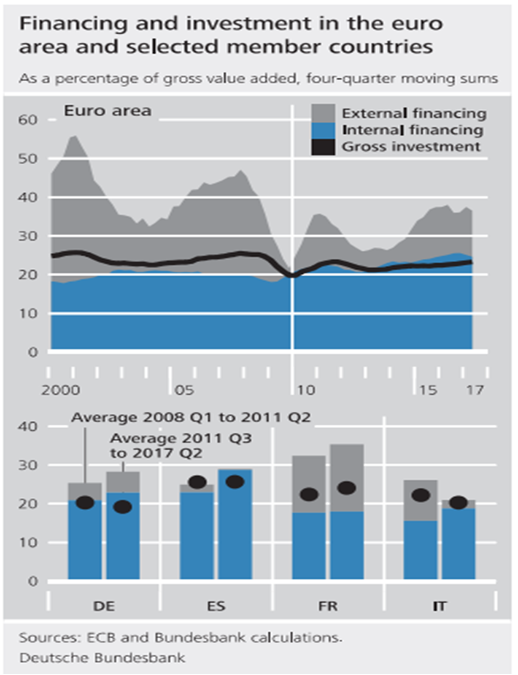

- First, there has been a shift away from funds raised externally (“External Financing”) to the use of surpluses generated through Corporates’ operations (“Internal Financing”)

- Second, External Financing has tended to experience a shift from borrowed capital to equity capital

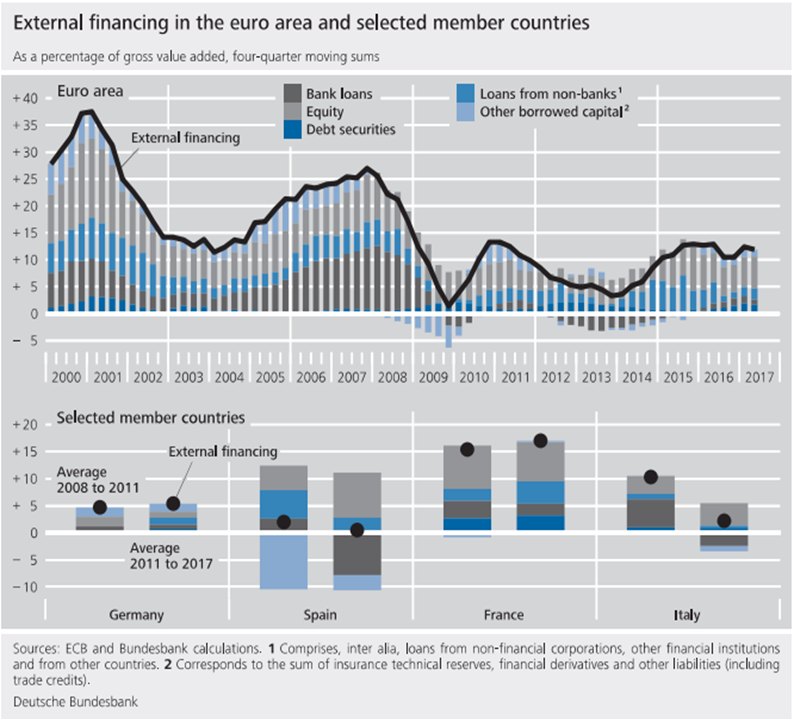

- Third, bank loans have lost some of their importance as a debt financing instrument compared with other forms of debt such as loans from non-banks and debt securities

External Financing:

- Shift from borrowed capital to equity

- Slight increase in leverage

- Substitution by debt instruments, i.e., (temporary) outflows for bank loans; at the same time, inflows of other debt instruments

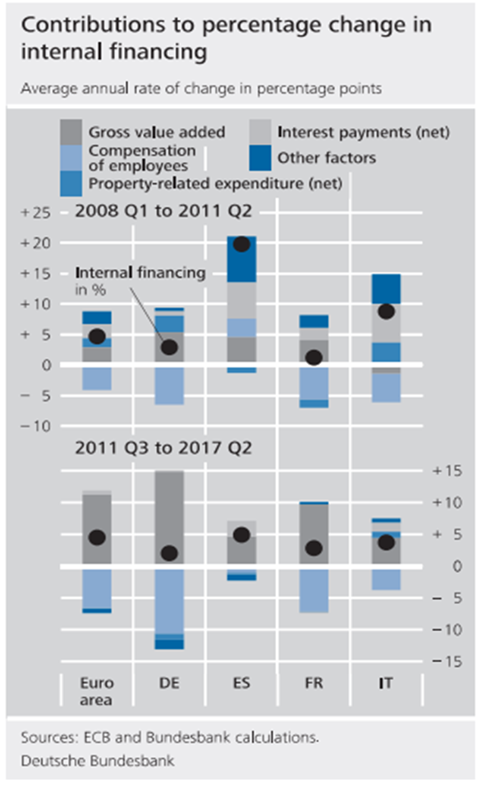

Internal Financing benefitted of significant contribution by gross value added in the past compared to other contributing components.

The shift towards a larger share of Internal Financing and equity financing combined with a more diversified debt financing structure is likely to help make the funding of Corporates going forward

Key elements to optimize components of financing Corporates and combining External and Internal Financing are:

- Monetizing account receivables, and

- To optimize working capital

Qube Financing anticipated these aforementioned development by designing & offering its alternative working capital finance solutions as its strategic mission:

- Substitution as part of External Finance using PRI® inside as well as PRI® Supply Chain and as such monetizing account receivables

- Reducing need for Internal Financing by using PRI® CrediSoft to optimize working capital